The Bonds of Reputation

How reputation underwrites trade, and the network science behind it.

Picture a pair of merchants quietly discussing the contents of a parcel at dawn. By noon, it will have changed hands multiple times, doubling or tripling in value, embedded in deals worth millions of dollars. And yet not a single contract will be signed, nor a dollar wired. These transactions will all be brokered on the simple notion that a man’s word is his bond.

While the scene reads like a romantic vestige of pre-industrial commerce, it unfolds every day in the financial capital of the world. In Midtown Manhattan, the largest diamond market in the world thrives: The Diamond District. The words that securitise transactions here are ancient, however: “mazel u’bracha”, a Yiddish phrase to convey ‘luck and blessing’.

The choice of words reflects the de facto monopoly that Jewish diamond merchants (‘diamantaires’) have long held in the industry. Their dominance is no historical accident; it is an institutional achievement. Over time, they have constructed a governance system that operates entirely parallel to the legal and financial systems they formally inhabit. It is a private order built on trust, where reputation is both collateral and a cudgel. And this network often rivals, if not eclipses, the bargaining power of nation-states.

What makes this network so effective is a set of institutions and social technologies that instantiate trust where opportunism is uniquely tempting. While contracts are the preeminent social technology for forging trust between counterparties, they are incomplete without the enforcement of terms and behaviour. The privately ordered governance mechanism in the industry enforces executory contracts more effectively than public courts, establishing it as the preferred venue for diamantaires.

The principles behind this governance mechanism are rooted in the Abrahamic tradition, where the act of contracting is not just a legal artefact but an ethical commitment underwriting your identity.

“If a man vows a vow to the LORD, or swears an oath to bind himself by a pledge, he shall not break his word. He shall do according to all that proceeds out of his mouth.” (Numbers 30:2)

The longest verse in the Qur’an is also devoted to the procedure for contracting a loan, explicating the earlier Abrahamic code as a communal responsibility.

O believers! When you contract a loan for a fixed period of time, commit it to writing. Let the scribe maintain justice between the parties […] Call upon two of your men to witness […] The witnesses must not refuse when they are summoned […] You must not be against writing ˹contracts˺ for a fixed period–whether the sum is small or great. This is more just ˹for you˺ in the sight of Allah [...] (Al-Baqara, Verse 282)

By requiring witnesses, the Qur'an transforms private dealings into socially embedded relational acts that inform collective memory, induce performance, and ultimately sustain the institutional architecture of a productive society.

Economic coordination depends on credible enforcement, and the best systems reduce the cost of trusting one another. Institutions cannot manufacture trust, but they can create the conditions for it to flourish. And societies that succeed in lowering the cost of trust unlock orders of magnitude more economic growth than societies that merely lower the cost of coercing one another.

Despite inheriting these Abrahamic accords, Muslim economies are in a situation where trust has been corroded by rent-seeking elites and rampant opportunism. Muslims searching for sovereignty in the 21st century are confronted with a fractured landscape. Debanking in the West, opportunism in the East, and a global economy that oscillates between over-regulation and lawlessness. The impulse, all too common, is to digitise institutions from the past. The solution, however, is not to return to the Golden Age but to initiate a golden age of governance, to evolve institutional protocols – social, moral, technical – for the world we inhabit and are entering, seeking sovereignty not in nostalgia but as a matter of stewardship.

To see why the innovation of social technologies is critical in the 21st-century Muslim search for economic sovereignty, we need to trace the arc from medieval trade networks to modern institutional substrates.

Reputation As Regulation

In the 11th century, a coalition of Jewish merchants, the ‘Maghribi Traders’, built what has become the seminal case study of what economists call ‘private ordering’. It was a lex mercatoria (merchant law) where transactions and disputes were governed by community norms and institutions, evolving in response to the environmental constraints and costs of maritime trade. Operating across the Mediterranean under Muslim rule, the Maghribi traders thrived under an imperial umbrella while avoiding reliance on state enforcement, owing to the broad legal autonomy granted by Islamic governance.

Contracts moved trade beyond the immediacy of spot exchanges, enabling what Charles Fried called ‘time-extended exchange’. This shift demanded deeper trust between parties, since promise and performance were separated. But these contracts were only effective to the extent that legal sanction was a credible threat, and that a court could enforce terms. But in the medieval Mediterranean, crossing political and legal boundaries, i.e. ‘space-extended exchange’, courts were either too costly or entirely toothless to provide these assurances. The Maghribi Traders recognised these limits and responded by building institutional networks that substituted the enforcement function, relying on courts only as a measure of last resort.

What developed was a network-based enforcement regime, where reputation acted as regulation. Deals were not just committed to writing, but etched onto the collective memory of the merchants. They created an information layer that transmitted market information (logistical data, prices abroad) and reputation-relevant information. These reports, requested by merchants, would detail a potential partner's past conduct and payment punctuality. The letters (preserved in the Cairo Genizah) moved swiftly and cheaply enough to anchor a multilateral trust calculus, making private ordering through reputation a credible bond.

Topology of Trust

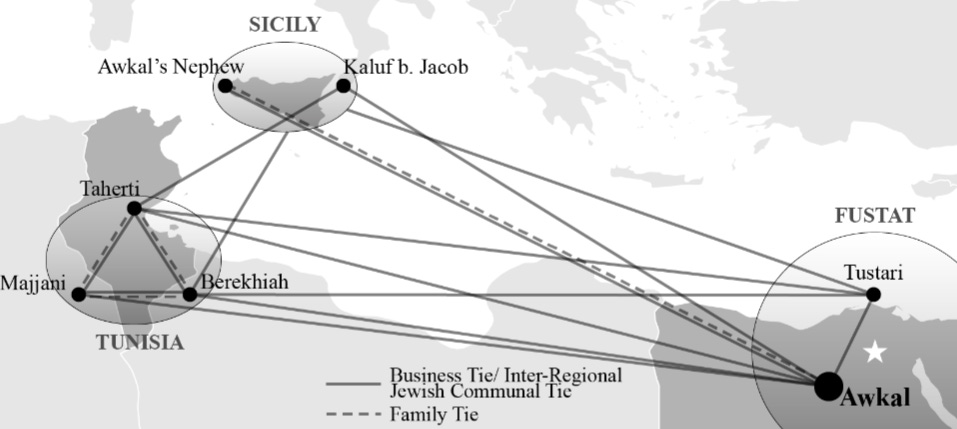

Understanding how this network functioned requires some network science. A small-world network is a particular network structure with two key properties: dense local clusters and relatively short paths linking distant nodes. While most nodes connect only to their immediate neighbours, the network's structure ensures that any node can access any other through a small number of intermediary connections. This is where the idea of “six degrees of separation” came from. This configuration enables information to travel efficiently across the entire network, even when individual participants are far apart and not directly connected.

The Maghribi network followed a classic bridge-and-cluster structure: tight-knit clusters of traders (‘cliques’ in centres like Fustat and Sicily) linked by a smaller number of bridges (strategic ties between prominent merchants spanning the Mediterranean). These itinerant merchants were the primary disseminators of information: merchants in clusters would consult these central nodes, who would access and relay reputation reports via letters to their inter-cluster ties. These information brokers had strong incentives to maintain accurate records of behaviour. Their own economic and social standing depended on being trustworthy disseminators, thus emerging a sort of meta-reputation. This network structure minimised information costs by reducing the intermediaries needed to verify reputation, avoiding the expense of constantly updating every trader. Yet it remained robust enough to ensure that defection or misconduct quickly became widely known.

The enforcement and governance of contracts were based on the credible threat of network exclusion. In the language of game theory, the present value of future pay-offs of cooperation inside the network far outweighed the payoffs of opportunism. The system also incentivised timely performance, as delayed shipments and payments also damaged reputation. Collective ostracism was a potent threat. A trader was not just excluded from a cluster, but from the entire network, effectively barred from trading anywhere in the Mediterranean.

All this matters because small-world networks are ubiquitous: power grids in the United States, the collaboration graph of film actors, and even the neural networks of the worm C. elegans exhibit small-world properties. Identifying the contract governance properties of small-world networks sets the stage for formulating how they can be a part of institutional foundations for trade in a variety of modern markets. Today, a highly evolved form of this Jewish private ordering mechanism, rooted in reputation and communal enforcement, continues to flourish in what is perhaps the most sophisticated legal forum on Earth.

The Diamond Dealers Club

Good name in man and woman, dear my lord,

Is the immediate jewel of their souls

– William Shakespeare, Othello Act 3: sc. 3

The New York Times called trust the real treasure of the Diamond District.

Diamonds are extracted from mines mostly in Botswana, Russia, and Canada; the product of immense heat and pressure deep beneath the Earth’s crust over billions of years, which compressed carbon into what is the hardest substance on the planet today. These diamonds are then shipped to trading centres around the world: Antwerp, Surat, and most notably, New York City. This is where the trade comes to life, where craftsmanship meets commerce, creating a $100 billion market.

But why is it that when you walk down 47th St, you suddenly hear Yiddish and spot yarmulkes?

Jewish predominance in the diamond industry is the product of a few forces. Firstly, the restriction on Jewish commerce in pre-Enlightenment Europe, including prohibitions on land ownership, membership of merchant guilds, and from traditional handicrafts, steered Jewish traders towards merchant professions with portable inventories. Secondly, some element of Jewish education, upbringing, and socialisation develops tacit knowledge and skills uniquely conducive to success in the diamond trade. And thirdly, ethnic cartels in general collude to maximise collective income, even at individual cost. By charging competitive prices to members and oligopoly prices to outsiders, rivals are priced out and the tribe flourishes.

Yet none of these explanations would have survived relentless market pressures. The real answer lies in something neoclassical economics largely ignored: the hidden costs embedded in every transaction. While economists focused on prices and quantities, a newer school called New Institutional Economics addressed transaction costs that organise commerce day-to-day. Every deal carries implicit costs that practitioners know intimately: finding trustworthy partners (search), negotiating terms (bargaining), ensuring people honour their commitments (monitoring and enforcement). The Jewish diamond network secured its hegemony by an institutional solution to enforce credit sales at transaction costs that competitors couldn’t match.

Credit Where Credit’s Due

Credit sales are essential in the diamond trade because they address liquidity constraints. Cash upfront would strangle the trade, given the price of diamonds and the turnaround imposed by the cutting process. Sellers also know that they can get significantly better prices for a stone by extending credit terms. In fact, trade credit is so central to the industry that it has been called an implicit capital market. Diamantaires can obtain credit from each other at a far lower cost than they could anywhere else, because as a network, they have more information about a buyer’s creditworthiness than any other lender in the world.

Yet, the temptations of opportunism and even outright cheating in this industry are unlike any other. Diamonds concentrate immense value in the most portable and untraceable forms, and thieves can cash out anywhere on the globe. While most industries can rely on the state’s legal machinery to compel performance, legal scholars have long noted the disability of courts here. As Richman notes, the failure of courts to prevent flight amounts to a failure to enforce the executory contract.

That is the notion this institutional machinery was built to solve: the extraordinary margins of trading on credit are matched by the magnitude of risk. And while cultural norms of fairness are necessary, they are insufficient to sustain the widespread multilateral cooperation observed. Rather, it is a governance mechanism, composed of a web of industry and communal institutions which anchor reputation and exert costly deterrents for defection.

In a market dependent on credit, they have developed social technologies that instantiate trust and govern agreements through the force of reputation. It is a private order based on enforcing contracts through staked reputation, mediating disputes through a private, mandatory arbitration system, and enforcing decisions through ultra-Orthodox community institutions.

The heart of this ‘institutional stack’ is the Diamond Dealers Club. The DDC functions as a consensus engine to reduce transaction costs among diamantaires and to instantiate trust. It first mediates entry, filtering for long-term cooperation rather than one-off opportunism. Entry is mediated either through family ties, Hasidic faith, or even prior dealings with a member, and this is where scrutiny is sharpest. An aspiring diamantaire, Tommy Van Scoy (a non-Jew) was admitted simply because he paid money back on time, but recalls that the DDC knew how much he paid for his mortgage every month and where his children went to school.

In this system of mutual reputation, a sponsor’s standing is tethered to the dealer they endorse. Their reputation can be enhanced or diminished based on the new dealer's conduct. Inside the highly secure trading hall of the DDC is “The Wall”, which displays photos and references of new entrants, announces the nomination of potential members and invites current members to comment on their trustworthiness.

When disputes inevitably surface, the Diamond Dealers Club fulfils its central role as an arbitration system. Court cases are exceedingly rare; membership is conditioned on mandatory arbitration and waiving your right to litigation. Panels of reputable diamantaires deliberate behind closed doors, and their decisions are final. Arbitration is faster and cheaper than court, and arguably more just. Experienced diamantaires streamline the evidentiary processes and assessment of damages far more accurately. Procedures are tailored for archetypical disputes, so costs are low and rulings swift. Rulings are then posted on the DDC’s public wall, and reputation-relevant information circulates to bourses worldwide.

A decision against you doesn’t spell exile but may prompt future partners to proceed cautiously, by offering tighter credit terms or requesting collateral. Only blatant fraud or refusal to honour an arbitration ruling leads to expulsion. The DDC’s arbitration establishes the immutable reputational record, and if that alone doesn’t compel compliance, community institutions enforce the club’s judgments.

The engulfing presence of Orthodox Jews has made it such that economic relationships are nested within the community itself: expulsion threatens business and belonging. Orthodox Jewish institutions consciously deter dishonest and opportunistic behaviour through coordinated sanctions. The DDC can even initiate proceedings in rabbinical courts, where penalties range from restricted access to synagogues through to formal excommunication. Whereas the Maghribi Traders cast merchants out of the trade network, the diamond industry ostracises them from society, forfeiting not only interlocking business ties but also access to matchmaking networks. So not only do defectors get their face plastered across the wall of every bourse and name emailed to every dealer around the world, they will be effectively severed from the ethnoreligious lineage by not marrying a Jewish woman.

Another force enables Jewish diamantaires to trust one another so extensively: social cohesion, or as Ibn Khaldun put it, asabiyya.

Fortunes Forged In Faith

The Maghribi Traders and the diamantaires exemplify the economic rewards and competitive advantages of transacting with your co-religionists. The inherent confidence woven into religious kinship dismantles the inherent scepticism that governs commercial exchange. Among co-religionists, the foundation of trust emerges pre-established, elevated beyond the cautious calculations that typically govern transactions between strangers. Within the Abrahamic framework, this heightened confidence springs from theological imperatives: believers orient their decision-making toward eternal consequences, extending their temporal horizon far beyond expedient material gains.

Interest, for instance, is a risk-management tool that places a premium on the absence of trust when money is lent. It is in that sense a tax on social cohesion, and trust is a discount rate on credit.

Individuals belonging to a distinct religious group also share tacit behavioural norms known in the Islamic vocabulary as adab and akhlaq. Institutions are more than just demarcative hierarchies and bylaws, operating on top of an intangible substrate of culture, norms, and shared mental models, all of which are instinctive to people operating from the same religious framework. In the case of the Maghribi Traders, operational norms became self-enforcing because of shared cognitive models. These mediate individual behaviour and structures interaction discreetly, creating the cultural operating system on top of which formal organisations can be built, and society shaped.

Opportunism & The Muslim Condition

Modern Muslim markets rarely enjoy this discount rate on credit. Court systems are slow, traditional institutions captured by rent-seeking elites, and corruption at the top cascades down into a low-trust society. The implicit premium on distrust means productive opportunities fall through since risk dwarfs reward, creating a vicious cycle.

While the priority for any Muslim political economy must be institutional reform, it is not sufficient. Conventional institutions are a floor, not a ceiling.

Changing this demands governance structures that can neutralise transaction hazards where opportunism thrives. Capital flows through the arteries of Western banks that can freeze it overnight. Censorship, surveillance, and debanking are not speculative fears but active policy. Owning infrastructure like payment rails, which are not subject to the whims of any party with the power to sever access unilaterally (and often arbitrarily), is necessary as a matter of sovereignty. Oscillating between intermediaries which would either stifle or censor productive enterprises, evolved forms of the privately ordered networks, such as the Maghribi Traders & diamantaires, may be essential for Muslims in the 21st century.

The 19th century offers Muslims a blueprint. The trust assurances of these reputational networks were not exclusive to the Jewish communities. Trans-Saharan caravan traders operating between West and North Africa crafted a remarkable synthesis of these two paradigms. These were merchants who organised primarily agency agreements to trade goods. Through their activities, private and public institutions became functionally integrated, with recognition of the scope where one approach was more useful and economical than the other.

These traders deployed whichever paradigm suited them best, utilising the efficiency of reputation-based networks while nesting them seamlessly within formal legal frameworks. Courts (or more accurately, judges) remained available when disputes demanded formal adjudication, but only as a last resort given the prohibitive costs of legal proceedings in time and money. The Trans-Saharan traders reveal that the optimal solution isn't choosing between private and public order, but building robust private networks that can govern most contracts while keeping formal legal systems as backup infrastructure when stakes or complexity demand it.

The key to successful economic exchanges here is not necessarily an impartial and efficient third-party enforcing agency, but the existence of a level of trust or other self-enforcing institutions in relevant networks of commerce [...] In other words, the state is neither necessary nor sufficient. The simple model in which it is only the state and threat of its justice and police systems that makes people behave cooperatively seems a poor description of any known situation.

– Joel Mokyr

The private order institutions highlighted here were not simply horizontal clusters constricted to a particular locality, but a type of network state, running parallel to but relevant in the political economies in which they were situated. The dispersed, diasporic state of Muslims today is ideal for forming such small-world networks, which emerge when distant connections yield high returns but transaction costs are high enough that strategic actors must bridge across clusters.

Trust is the subtle architecture of prosperity, but it rarely emerges on its own. It must be carefully cultivated through social technologies and institutions that make trust both possible and profitable through the bonds of reputation, which underwrite all productive societies.

Author: Haseeb Ahmed is based in Toronto. After driving growth operations for several startups, he is now working on transaction scripts and payment infrastructure. He is interested in the future of firms and money. You can follow his ongoing experiments and reflections @haseebinc.

Artist: All art has been custom-drawn for Kasurian by Ahmet Faruk Yilmaz. You can find him on Instagram and Twitter/X at @afaruk_yilmaz.

Socials: Follow Kasurian on social media via Substack Notes, Instagram, and Twitter/X for the latest updates.

Further Reading

Barak Richman, How Community Institutions Create Economic Advantage

Lisa Bernstein, Contract Governance In Small-World Networks

Joel Mokyr, The Institutional Origins Of The Industrial Revolution

Ghislaine Lydon, Contracting Trust

Primavera De Filippi, Blockchains and The Economic Institutions of Capitalism

Oliver Williamson, Transaction-Cost Economics: The Governance of Contractual Relations

Ronald Coase, The Problem of Social Cost